Robert Kiyosaki is well known for his famous book “Rich Dad Poor Dad”. In the book, he discusses what he learned growing up from his father and whom he calls his second father. One dad whom he called his “Poor Dad” taught him the traditional way to get by – “go to school, get a degree, get a good job, save for retirement..” etc. We’ve all heard it. His “Rich Dad” taught him the basics of money, how it worked, and how to make it work for him to become wealthy.

I will muster the energy to write up a review for rich dad poor dad too in the coming days, depends on how busy our vacation goes. We are currently in Dallas on a family trip as I sneakingly write this post.

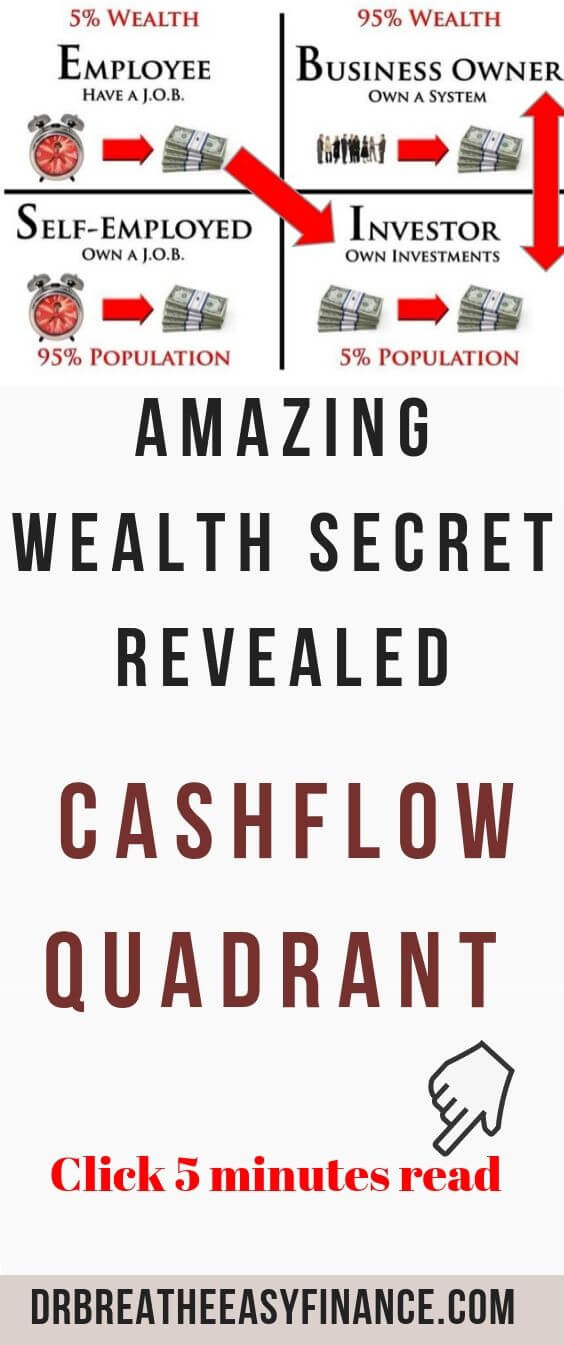

Cashflow Quadrant is a further explanation of the concepts his Rich Dad taught him about money. It dissected different types of way to make money and separates them into different categories which are:

- Employee

- Self-Employed

- Business Owner

- Investor

Robert Kiyosaki explains the differences between the four types of employment, and how they can affect your financial future. This book review of Cashflow Quadrant (summary) lays out the short version of what you can learn and why it matters to you financially.

A quick primer on youtube about the cashflow quadrant. It is quite popular. You might want to skip the first minute to get to the meat of the talk.

I really think everyone needs to read this book and understand the concept / I mean really understand it. If you want to buy it, here is a link for you below.

Table of Contents

The 4 Cashflow Quadrant Employment Categories

The traditional money game, as briefly mentioned above and taught in Rich Dad Poor Dad, leads people to employment that falls under the “Employee” and “Self Employed” categories, also referred to as “E” and “S” sides of the Cashflow Quadrant (see image below).

Some of us may fit into different employment types than others, and some just simply might not have any desire to be a part of others, such as owning their own business. Regardless, one thing stands true; a larger portion of wealthy individuals and families make their money from employment that falls under the “Business Owner” and “Investor” categories, also referred to as “B” and “I” in the book.

What are the main differences between the four categories of employment, and how do they apply to build wealth?

Robert Kiyosaki learned from his Rich Dad that in order to build wealth, creating processes and systems to work for you is the most efficient way both in terms of time and money. In other words, by being able to create different forms of passive and semi-passive income, your wealth will grow exponentially faster than depending on one income stream. The following descriptions of each of the four employment categories are laid out in detail below, and how they apply to building wealth, as taught by Robert’s Rich Dad.

How Being An“Employee” Category Is A Slow Path To Wealth

Employees are anyone who has a boss and gets paid by another individual or company. Robert’s Rich Dad taught him that this is a slow path to wealth. Why? Because anyone that falls into the “Employee” category has little control over how much they get paid in proportion to how hard they work. Sure you can work hard and hope for an eventual raise or promotion, but a 5% raise or promotion is no fast track to growing your income.

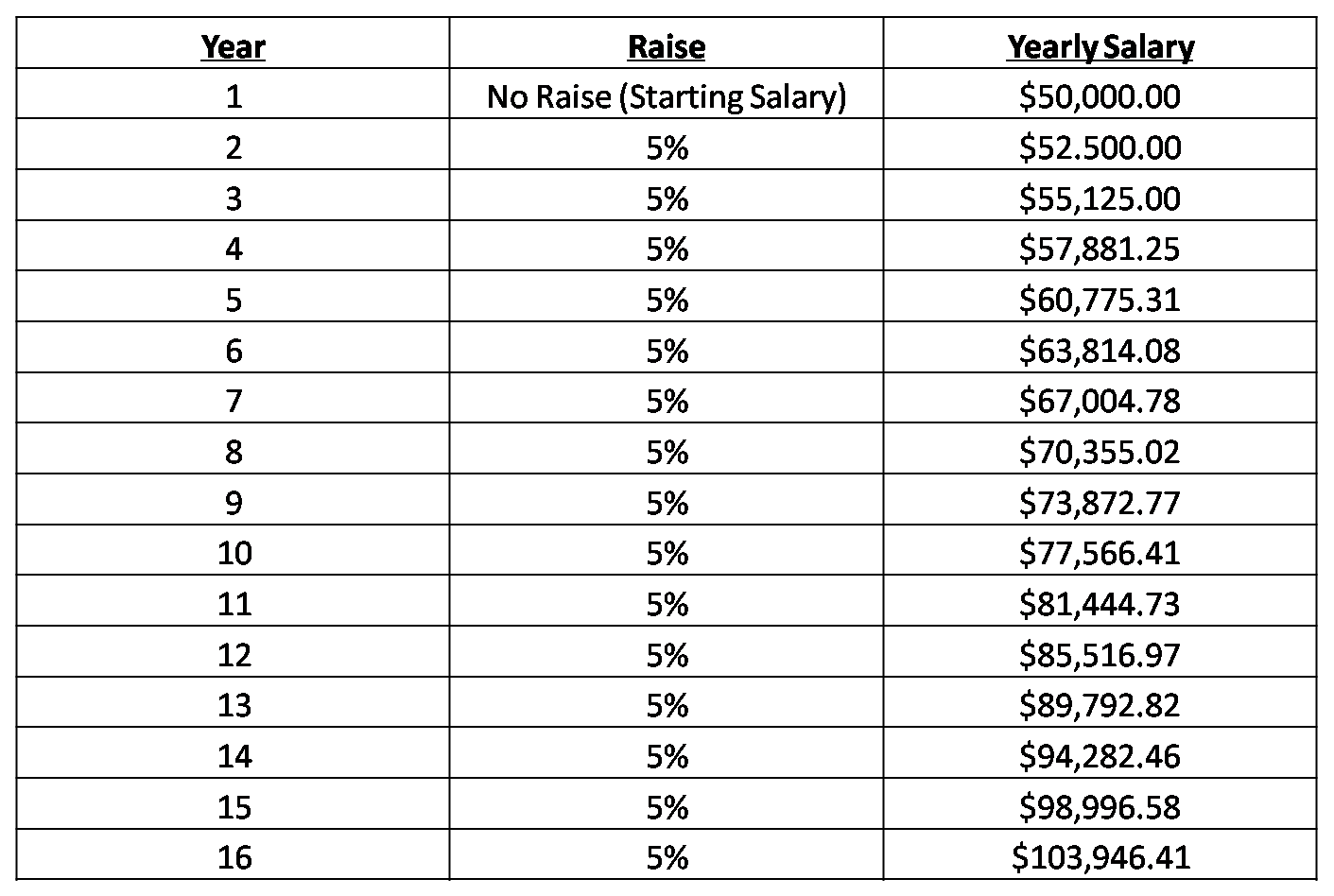

Let’s say you start out getting paid a salary of $50,000 per year. You anticipate you can get a 5% annual raise; how long will it take you before you start making a 6 figure income? It will take you a total of 16 years with a salary increase of 5% per year before you make at least $100,000 per year. That’s nearly half your career! (see the table below)

Don’t get me wrong, most people start here. Majority of my income is still from being an employed doctor. The important thing is to find ways to move to the higher yield cash flow categories and reduce the percentage of your income that is dependent on being an employee.

The important thing is to find ways to move to the higher yield cash flow categories and reduce the percentage of your income that is dependent on being an employee. Share on X

If your plan is to build wealth as fast as possible, this is perhaps your slowest path, and you should expect to work the greater part of 40 – 50 years to save enough to retire. Keep in mind, by no means does this mean it’s not a good choice. Some of you out there may be completely satisfied with that income and would rather work a long career and retire in your older age. But if your plan is to build wealth, being an employee is not your best option to get there.

Can You Build Wealth Being “Self Employed?”

The second category of employment is the “Self Employed” individuals, and Robert Kiyosaki advises against this option as well. If you don’t have a direct boss, but you are an individual contributor running the show of your business, then you fall into this category. This includes local small business owners, contracted employees, freelance workers, and anything related. As long as the business cannot go on without you, you might call yourself fancy names like CEO, but you are still self-employed.

A common example of this is a doctor who works as a consultant as a locum, a one physician private practice falls under this category too. If you die or fall sick, chances are, the business will not be able to continue.

Blogging, for the most part, is also another great example. If the owner belly up, usually, it is difficult to maintain.

Why is being “Self Employed” not a top choice to build wealth?

The problem laid out in Cashflow Quadrant is that being a small business owner of any sort, ties you directly to your business. That means you have to directly trade your time, in order to keep making money and building wealth. Although this provides more flexibility than being an “employee” of a company, it still has its limits and obligations in order to keep the income flowing and growing.

For example, an insurance agency owner may be their own boss, choose their own hours, and can hire employees to help with the workload, but the fact is that the agency doesn’t progress and grow without his or her direct involvement. There comes a point when a small business outgrows the term “small” and begins entering the “Business Owner” category, which is certainly a possibility for a small local insurance agency. But until it’s large enough to be bringing in tens or hundreds of millions of dollars, it’s likely going to require the business owner’s direct involvement to maintain.

How To Build Wealth Fast By Being A “Business Owner”

What’s the difference between being self-employed and being a “Business Owner?” You are a business owner when you provide the financial backing to run the business but doesn’t require any direct involvement on a regular basis to maintain. You have hired out executive positions to oversee and manage the company operations, and your involvement is no more than a regular “board meeting” to communicate with the hired executives and make executive decisions.

Being a “Business Owner” is a true form of passive income, and exponentially accelerates your progress to building substantial wealth. In essence, you have built a machine that can operate without your management and makes you money without taking your direct time. Robert Kiyosaki’s Rich Dad taught him that true wealth is built when you can hire employees to run the show for you and still make money while you sleep and is perhaps one of the top lessons taught when you read Cashflow Quadrant.

The B quadrant is my long term goal. I will encourage you to think big and not stop at being an employee or self-employed but take steps to cross over to the B category.

Investing Is Passive Income In Its Truest Form

The fourth category of employment or making money is the Investor quadrant as explained by Cashflow Quadrant. The overall process to building wealth as Robert’s Rich Dad taught him, is to find out how to multiply your time and money without your direct involvement, or in other words, to create true forms of passive income.

Investing in companies both privately and publicly traded companies takes no more than some discretionary money to start investing and building wealth. By purchasing stock in companies, you can make money while you focus your time and efforts on other areas of importance like spending time with family, evaluating large decisions to be made as the owner of multiple businesses, or, really, anything you want!

Investing is a fast path to wealth because it’s like planting a seed now, with the expectation of reaping the rewards in the near future. One seed can grow over time to produce years and years of fruit to live on.

A major part of this blog focus on investing. I do invest in stocks currently and gearing up to dabble into real estate. So join us on the adventure and start investing today. Start sowing the seed right now.

Here are some blog posts to get you started.

The importance of time value of money – an entertaining post on why you need to invest today as the dollar at hand now is worth more than dollars in the future.

The rule of 72 let you know when you will double your money – I even did the mathematical derivation of the equation here. I know I can’t believe myself either.

4 investing ideas for the absolute beginners

Why the 3 fund portfolio is all you need.

How to become a Roth IRA millionaire

Cash drag is the enemy of investment growth, and how to decrease the effect of cash drag on your portfolio

6 basic steps to start investing

The end to the debate of all time – Do you need bonds in your investment portfolio? The article answers all your burning questions.

Free stock trading platform review – Webull. No trading fee!!!

Who Should Read Cashflow Quadrant by Robert Kiyosaki?

Having a healthy bank account to some people may not even have a price tag. Being able to build that financial nest egg to rely upon without the need of a job is an achievement that not many are able to obtain. Cashflow Quadrant, however, provides a proven process and detailed explanation on how this can be achieved. All it takes is the willpower and trust on our part to determine if it’s a pursuit worth working towards or not.

If that sounds like you, then you will love Cashflow Quadrant, and perhaps other popular books by Robert Kiyosaki like Rich Dad Poor Dad. You can grab the rich dad poor dad book right now. You can also use the same link to search for any of Robert Kiyosaki book that interests you.

Cashflow Quadrant is a great read for entrepreneurs, founders, and creative minded individuals who like seeking new ways to build and grow their wealth. It isn’t, however, a book on personal finance and how to properly budget your way out of debt. Its focus is on bigger goals and aspirations that come after the basic personal finance fundamentals are mastered and can serve as a turning point to your financial future.

What Worked Yesterday May Not Work Today…

Robert Kiyosaki’s “Poor Dad” taught him that he needs to go to school, get an education, get a good job and save for retirement. The problem with this is that his Poor Dad was living paycheck to paycheck and had little to no time for family. While this was the traditional norm years ago, its apparent things have changed a little, to say the least, and often times requires more than just a good education. It takes understanding and learning how money works, how to make your money work for you to grow wealth, and you can learn how in Cashflow Quadrant.

Last chance to grab a copy.

Don’t forget to join us to get more awesome personal finance tips and grow with us as we explore how to become financially independent.

I am a pulmonary and critical care doctor by day and personal finance blogger/debt slaying ninja by night.

After paying off close to $300,000 in student loan debt in less than 6 months into my real job, I started on a mission to help others achieve the same. There is no magic to this than to strap up and get it done. Some of the ways we achieved this include side hustle, budgeting, great negotiation skills, and geographical arbitrage.

When I was growing up, common knowledge in Nigeria is that there is one thing you cannot trust anyone else with, and you guessed it – your money.

Being frugal came easily to me based on my background. However, the concept of building wealth did not solidify in my mind until when I finished medical school. I wish I knew what I know now when I was 14. Still, I don’t know enough and I am constantly learning to improve my knowledge.

My goal is to reduce financial illiteracy among young professionals. I am catering to the beginners – babies and toddlers in financial literacy.

Leave a Reply